A standard Wiener process (often called Brownian motion) on the interval

![]() is a random variable

is a random variable ![]() that depends continuously on

that depends continuously on

![]() and satisfies the following:

and satisfies the following:

For use on a computer, we discretize the Wiener process with a timestep

![]() as

as

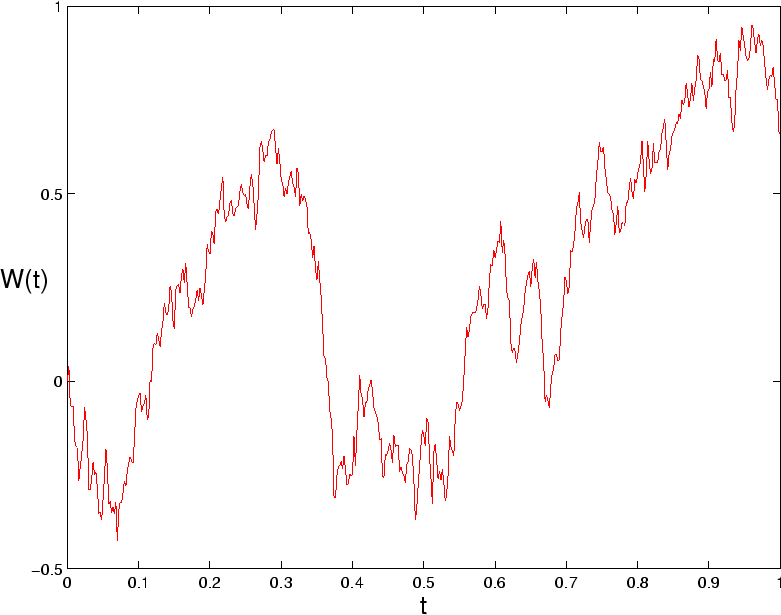

The article by Higham gives two equivalent Matlab programs to calculate a realization of a Wiener process. First bpath1.m:

%BPATH1 Brownian path simulation

randn('state',100) % set the state of randn

T = 1; N = 500; dt = T/N;

dW = zeros(1,N); % preallocate arrays ...

W = zeros(1,N); % for efficiency

dW(1) = sqrt(dt)*randn; % first approximation outside the loop ...

W(1) = dW(1); % since W(0) = 0 is not allowed

for j = 2:N

dW(j) = sqrt(dt)*randn; % general increment

W(j) = W(j-1) + dW(j);

end

plot([0:dt:T],[0,W],'r-') % plot W against t

xlabel('t','FontSize',16)

ylabel('W(t)','FontSize',16,'Rotation',0)

Next bpath2.m:

%BPATH2 Brownian path simulation: vectorized

randn('state',100) % set the state of randn

T = 1; N = 500; dt = T/N;

dW = sqrt(dt)*randn(1,N); % increments

W = cumsum(dW); % cumulative sum

plot([0:dt:T],[0,W],'r-') % plot W against t

xlabel('t','FontSize',16)

ylabel('W(t)','FontSize',16,'Rotation',0)

These programs produce Figure 1.